Jessica Ullom-Minnich & Hanna Venera

In the forty years leading up to the COVID-19 Pandemic, China’s GDP grew reliably. Between 1990 and 2007, it doubled every seven years, on average (Blanchard, 2017, p.14). Even during the global recession of 2008-2009, GDP growth only dipped to 9.4% annually, even though the country was highly affected by the reduction in demand for its exports (Blanchard, 2017, p.14). However, in recent years, the astronomical growth has begun to slow. Between 2010 and 2014, growth averaged 8.6%, substantially above that of the US, but still showing a larger trend (Blanchard, 2017, p.14). This gradual slowing of high GDP growth could have a number of meanings. First, it is likely a natural advancement in the country’s economic maturity. China’s growth was, for a long time, the direct result of a high investment rate, 48% (Blanchard, 2017, p.14). However, as the economy evolves, it begins to “rebalance, meaning that the share of consumption to GDP is increasing and the share of investment to GDP is decreasing,” (Sznajderska, 2019, p. 1574). The slowing of China’s growth does not necessarily mean that the economy is in trouble, or even doing worse; it could simply be healthy progression. On the other hand, the reduction in growth could be the start of a contractionary period as cited in Liu et al. (2020), which would follow a more natural cyclical pattern. This explanation is particularly interesting in the context of COVID-19, because of the widespread policies in place as a response to the pandemic, including government shutdowns and stimulus distribution. Examining these two factors in concert, Liu et al. (2020) also argues that “recessions that coincide with the contraction phase of a financial cycle are especially severe,” the onset of the COVID-19 pandemic worsened the effects of China’s shrinking GDP growth (Liu et al., 2020, p. 2260). This would further explain the drastic dip in China’s GDP after a dynasty of growth.

To more closely examine the implications of an overlap between a contractionary period and COVID-19, it is important to examine the impact on GDP directly. During the first few months of the pandemic, China saw decreases in consumption, including a 16% decrease in retail sales, and investment, including a 23% decrease in residential sales (Cheng, 2020, paras. 5-6). More worrying was the prospect of decreased demand for exports by countries like the United States who were also suffering economically (Cheng, 2020, para. 14). As “China has grown into the largest exporting country in the world” in the past several decades, decreased demand made a large mark of the Chinese economy (Liu et al., 2020, p. 2271). In the previous US recession in 2008, China was spared the negative effect of a decrease in export demand by compensating for a large increase in government spending (Blanchard, 2017, p.14). However, without a renewal of this policy, loss of exports is once again a substantial threat to China’s GDP, and caused China’s GDP to drop significantly in the first few months of the pandemic. Overall, Liu et al. (2020) explains that “the Chinese gross domestic product has plunged 6.8% year on year in the first quarter of 2020… [which] is the first time in four decades that China has seen its economy shrinking” (Liu et al., 2020, p. 2260). This is notable due to its striking departure from the previous pattern of extreme growth, and indicates just how drastic the impacts of this pandemic will be (and have been) globally.

China's virus-hit economy shrinks for first time in decades. (2020, April 17). Retrieved from https://www.bbc.com/news/business-52319936

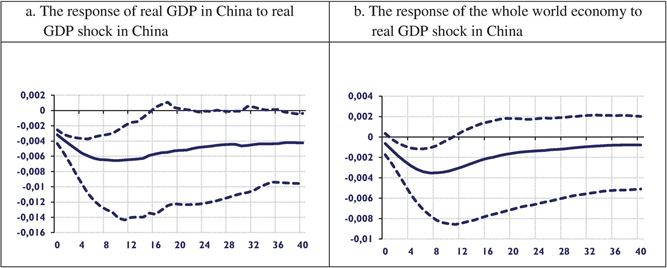

In the world of globalization, significant changes in the GDP of a country like China do not come without ripple effects. Because China is so intertwined with other countries, both as an exporter to nations like the US and an importer to poorer nations across South East Asia, the GDP shock that China experienced has potential to rattle other nations. In a study by Sznajderska (2019), a 1% decrease in the real GDP of China would produce, in the short term, a .23% decrease of real GDP globally (p. 1575). In poorer nations that depend on China as an importer of their goods, the decrease will likely be closer to .5% (Sznajderska, 2019, p. 1579). That means that, with China’s GDP down 6.8%, some nations could expect a more than 3 % GDP contraction, excluding economic contractions caused by COVID-19 in their own nations. However, it is important to note that even though China experienced a more drastic change in comparison to previous years, on the global stage, they are doing comparatively well. Real GDP growth in China from 1993 to 2020 (using quarterly data) indicated an average growth rate of 9.5% with a standard deviation of 3.6%, meaning that it is “quite high and relatively stable” (Liu et al, 2020, p. 2266). These numbers account for the decline in the first quarter of 2020, meaning that it was a relatively small shift, though it is still noteworthy that the pandemic caused a disruption in the pattern of growth. Further, China’s GDP in the third quarter of 2020 was about 5% higher than that of 2019, even in the context of the pandemic, which indicates that the government may have managed the crisis better than other countries through mandates, stimulus, and other resources (Anonymous, 2020, p. 74). This suggests that risk of China’s GDP shock affecting other nations is actually relatively low and decreasing as GDP continues to recover. While the long term trends of China’s economy (whether by contraction or natural evolution) are still somewhat up for debate, the striking decrease of GDP in the past year, by itself, is not concerning.

Sznajderska, A. (2019). The Role of China in the World Economy: Evidence from a Global VAR Model. Applied Economics, 51(15), 1574–1587. https://doi-org.ezproxy.plu.edu/http://www.tandfonline.com/loi/raec20

Works Cited

Anonymous (2020). Free exchange: The notorious GDP. The Economist, 437(9218), 74.

Blanchard, O. (2017). Macroeconomics (7th ed.). Pearson, 14.

Cheng, J. (2020). China Records First Ever Contraction in Quarterly GDP on Coronavirus; GDP contraction of 6.8% foreshadows pain likely to be reported world-wide. Wall Street Journal.

Liu, D., Sun, W., & Zhang, X. (2020). Is the Chinese Economy Well Positioned to Fight the COVID-19 Pandemic? the Financial Cycle Perspective. Emerging Markets Finance & Trade, 56(10), 2259–2276. https://doi-org.ezproxy.plu.edu/10.1080/1540496X.2020.1787152

Sznajderska, A. (2019). The Role of China in the World Economy: Evidence from a Global VAR Model. Applied Economics, 51(15), 1574–1587. https://doi-org.ezproxy.plu.edu/http://www.tandfonline.com/loi/raec20